Healthcare Just Got Trickier For Early Retirees

The “One Big Beautiful Bill Act” passed on July 4th, 2025 introduced sweeping changes to our tax code, however, it did not extend the enhanced health insurance subsidies available through the Marketplace.

That’s a big deal, especially for anyone planning to retire before becoming eligible for Medicare, or those already retired (but not yet 65).

So, beginning in 2026, the expiration of the enhanced Affordable Care Act subsidies have the potential to make early retirement health insurance very expensive for some, especially those without a solid plan in place.

First, What is “The Marketplace”?

Before I dig into this, I wanted to make sure everyone is on the same page about the Marketplace.

The Affordable Care Act established health insurance “marketplaces” in each state, creating a place where individuals without employer-sponsored coverage (or those who retire before becoming eligible for Medicare) can shop for and enroll in health plans.

The nice part was that subsidies were offered to individuals and families with incomes below a certain threshold, helping to lower monthly premiums and make coverage more affordable.

Which, most retirees see a drop in income when they retire so this is perfect.

Household assets have no bearing on the amount of subsidies a family can receive.

But, prior to 2021, there was a set income cap. Exceeding that income cap (even by $1), meant losing all available subsidies for the entire year.

What are the Enhanced Subsidies?

During the COVID years, various stimulus bills were passed which expanded the amount of subsidies that were offered. They also removed the income cap.

With no income cap, these subsidies would gradually decrease as a household’s income increased, until they eventually went to $0.

So there wasn’t necessarily a big “penalty” for your income being too high.

The provisions from these bills kept getting extended; the most recent extension going until the end of 2025.

Planning for 2026 and Beyond

Unfortunately, the “One Big Beautiful Bill Act” did not further extend those enhanced subsidies so that means the old income cap will be returning in 2026 and subsidies may be getting smaller.

The income cap is equal to 4x the Federal Poverty Level (FPL) which is determined by how many individuals are in your household.

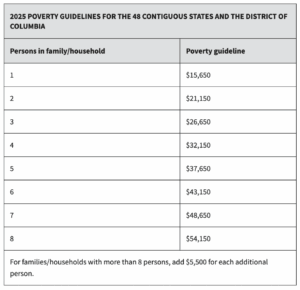

Here are the current 2025 Federal Poverty Levels:

Source: Department of Health and Human Services (https://aspe.hhs.gov/topics/poverty-economic-mobility/poverty-guidelines)

So for a retired husband and wife, 4x their Federal Poverty Line would be $84,600 in income ($21,150 x 4).

Remember, even earning $1 over this cap means you’re ineligible for subsidies and you bear the full cost of health insurance.

So What Do You Do?

Detailed retirement income planning will be a MUST for anyone planning to retire before Medicare age. It’s crucial to try to keep your gross income as low as possible until you can start your Medicare.

You’ll need to be very thoughtful about where you will draw your income from.

Here are some things to consider as you think about your retirement income plan:

- Consider what account(s) you draw from first

- Consider how you manage your household cash/savings to help minimize taxable income

- Consider delaying Social Security – with the income cap returning, it may not make sense to collect before you start Medicare.

Remember, withdrawals from IRAs/401ks/403bs are fully counted as taxable income. Distributions from Roth IRAs are generally tax-free*.

It’s also going to be incredibly important to have a tax-efficient investment strategy.

If you have a taxable brokerage account, you’re required to pay tax on dividends, interest, and capital gains as they’re earned; so before you retire, try to get this type of account as tax-efficient as possible.

- Minimize dividends

- Minimize interest

- Minimize or avoid capital gains, or offset any gains with losses (to the extent possible)

Certain mutual funds can send out surprise capital gain distributions towards the end of the year. So, depending on the amount you have invested in there, this is something that could easily derail your yearly healthcare plan.

Lastly, if you’re considering selling a rental property, taking a lump sum pension, doing a Roth conversion, working part-time, etc., the year you do these things could affect your subsidy eligibility.

Spreading income over multiple years or doing these things before retirement (if possible) could possibly help smooth out the impact.

Bottom Line

With the return of the income cap (aka “subsidy cliff”) and smaller subsidies in 2026, they’ll likely be less wiggle room when it comes to managing healthcare costs.

Thoughtful income planning and forward-looking tax planning will be critical. The right strategy can help you maximize subsidies and keep your retirement on track.

I hope you find this information helpful. Please reply to this email if you have any questions!

To your next adventure.

Need Professional Retirement Planning Help?

Schedule a Free Retirement Review

Learn how to lower taxes, invest smarter, and maximize your retirement.

Disclaimer: None of the information provided herein is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement, of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. The content is provided ‘as is’ and without warranties, either expressed or implied. Next Adventure Financial LLC does not promise or guarantee any income or particular result from your use of the information contained herein. Under no circumstances will Next Adventure Financial LLC be liable for any loss or damage caused by your reliance on the information contained herein. It is your responsibility to evaluate any information, opinion, or other content contained.

Welcome to the Next Adventure Financial blog where I share relevant info and educational content designed to help you have a comfortable retirement.

About the Author

Cody Lachner, CFP®, EA is a fee-only financial planner based in Lafayette, IN serving clients locally and virtually nationwide. Cody works with families approaching retirement and takes a tax-focused approach to retirement planning. His goal is to help families retire with confidence while lowering their lifetime tax bill.

We send out our Retirement Essentials newsletter every Wednesday which is full of information on retirement, taxes, and investing. This newsletter has plenty of content that doesn’t always make it into the blog.

Sign up below if you’d like to receive a copy!